Koon Yew Yin 7 March 2021

Hengyuan’s share price chart is up trend and it has reported increased profit in the last few quarters. Its EPS for quarter ending Dec was 57.17 sen and its previous EPS was 51.64 sen. Its last traded price was Rm 5.58 per share. Its average EPS per quarter was 54.4 sen. Its annual EPS will be 54.4 X 4 = Rm 2.18. It is selling Rm 5.58 divided by Rm 2.18 = 2.6 PE ratio.

Many investors would have bought it and expect to make a lot of money. I also bought it a few months ago and I sold it when I realized its revenue or sale of its refined product is being reduced due to Covid 19 movement control.

There are less vehicles travelling and less aeroplanes flying. As a result, its sale revenue is reduced and profit will be reduced.

In fact, someone told me that his wife who works for an insurance company told him that Hengyuan has to buy additional insurance for the ship carrying crude oil which is being delayed at the port. Hengyuan’s storage tanks are all full and cannot contain the oil from the ship because it cannot sell its refined fast enough to pump the oil from the ship.

Most investors know that petroleum price has been going up due to a number of reasons. As a result, Hengyuan’s stockpile of crude oil would have appreciated in value which can be considered as profit. Unfortunately, its sale of its refined products is being reduced due to Covid 19 movement control.

If you want to know more about Hengyuan, you can see the following from Hengyuan’s website and its annual report.

HRC’s complex oil refinery in Port Dickson has a licensed production capacity of 156,000 barrels per day. The major operating units in the refinery consist of two crude distillers, a long residue catalytic cracker (LRCCU), two naptha treaters and a merox plant, two reformers and a gasoil treatment plant. It also produces a comprehensive range of petroleum products including liquefied petroleum gas (LPG), gasoline, diesel, aviation fuel, fuel oil components, and chemical feedstocks like light naphtha and propylene.

Approximately 85 percent of these refined products are sold in Malaysia.

Our products are predominantly distributed using the multiproduct pipeline (MPP) to the Klang Valley Distribution Terminal (KVDT) and the Kuala Lumpur International Airport (KLIA). We also despatch products via road to more local users and via sea to more remote Malaysia locations including Sabah and Sarawak. Our significant customers for main fuels are Shell Malaysia Trading Sdn Bhd and Shell Timur Sdn Bhd, with whom we have entered into a 10 year term Product Offtake Agreement (POA), securing our sales of gasoline, aviation fuel and diesel in the country. This POA commenced in 2016.

Products such as propylene and light naphtha are exported out of Malaysia to be used as chemical plant feedstock and a portion of our LPG is exported to end users. In addition, we import gasoline components such as MTBE and additional LRCCU feedstock when the economics are favourable.

Let me tell you more about the sale of petroleum products from my own experience.

I the early 1960, US Government passed the anti-trust monopoly law. As a result, Standard Vacuum Oil Company had to separate its sale outlets into 2 divisions, namely Mobil and Esso stations.

In Malaysia all the existing petrol stations had to be renamed as ESSO stations and they had to construct new Mobil stations. I was appointed as an Engineering consultant.

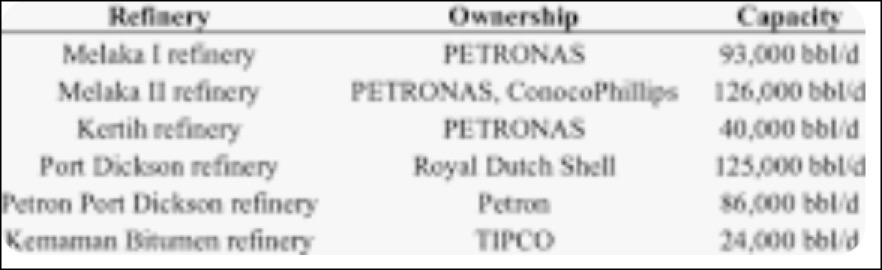

There are 6 refineries in Malaysia as shown on the table below.

An oil refinery cost a lot of money. That is why all the petroleum companies co-operate among themselves.

For example, Caltex has 420 petrol stations in Malaysia but it does not have a refinery. But Caltex can borrow or take the refined oil from any of the 6 refineries to sell at its 420 petrol stations.

Each petroleum company has petrol stations in every town and city. But each of them does not have refineries in every state.